The Global Forest Industry in the 1Q/2015

Global Timber Markets

• Sawlog prices inched up in the local currencies but fell in US dollar terms throughout

the world in the 1Q/15.

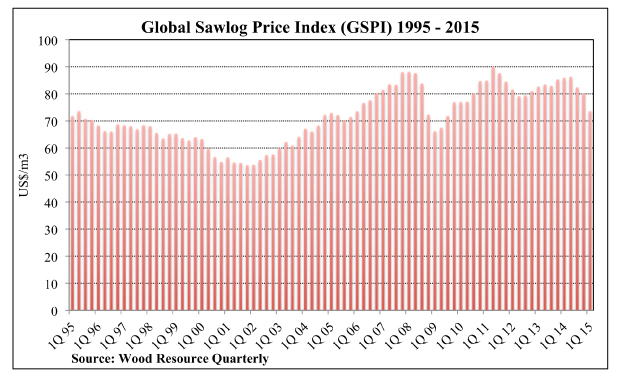

• The Global Sawlog Price Index (GSPI) fell by 8.2%, to its lowest level since the 3Q/09.

• Global trade of sawlogs slowed in early 2015, with the biggest declines in importation occurring in China and Japan.

• Japan has for many decades been a major importer of logs, but over the past few years the country has also started to export logs thanks to the weak yen.

Global Pulpwood Prices

• The stronger dollar, together with no or modest downward price adjustments of both chips and pulplogs in the local currencies, resulted in lower wood costs in US dollar terms in practically all major wood markets around the world.

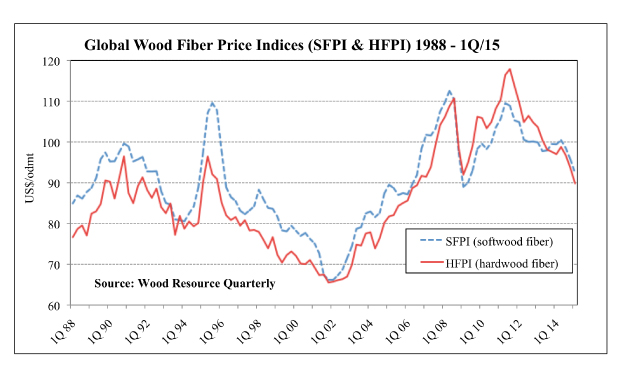

• The Softwood Fiber Price Index (SFPI) fell to $92.40/odmt in the 1Q/15, which was a decline of 3.5 percent from the previous quarter and 7.1 percent lower than, in the 1Q/14. The current SFPI is at its lowest level since 2009. The biggest prices declines occurred in Russia, Germany, France, Brazil and the Nordic countries.

• The Hardwood Fiber Price Index (HFPI) declined 4.0 percent from the 4Q/14 to the 1Q/15 to reach a nine-year low of $89.86/odmt. Wood fiber prices fell in 2 practically all regions outside the US with the biggest declines seen in Russia, Germany, Spain, the Nordic countries and Australia.

Global Pulp Markets

• This year has started out on a positive note for pulp producers, with global market pulp production being eight percent higher than during the first two months of last year.

• With prices for softwood pulp falling and hardwood pulp prices increasing so far this year, the gap between the two pulp grades has narrowed to less than $100/ton, the

lowest discrepancy since late 2013.

Global Lumber Markets

• Global lumber trade continued to rise in early 2015 with shipments being almost ten percent higher than in the 1Q/14. Most of the trading activities were in North America and Western Europe, while imports to Asia was down.

• Despite housing starts being lower in the 1Q/15 than in the 4Q/14, lumber production in the US increased slightly during the first three months of the year.

• Canadian lumber production was higher in early 2015 than in late 2014 despite weaker demand in all the three major export markets, the US, China and Japan.

• Lumber prices in the Nordic countries have fallen substantially since last summer in US dollar terms. The price decline in Finland and Sweden from August to February was 18% and 22%, respectively. Current price levels in both countries are at their lowest since 2009.

• With the decline in the value of the Rouble, Russian lumber has been become more competitive. In dollar terms, the fall over the past 15 months has been about 27% and

in Euro terms, just over eight percent.

• Demand for softwood lumber in China has really taken off this spring with import volumes doubling from February to April.

Global Biomass Markets

Exportation of wood pellets from North America to Europe and Asia reached an alltime high rising 22 percent in 2014 from the previous year.

Lower demand for pellets in Central Europe resulted in lower prices for residential

pellets during the spring. Average prices for pellets were down in both Austria and

Germany to their lowest levels in over three years.